Choosing the right health insurance policy in India is important to ensure proper medical coverage and financial security.

Health insurance kaise choose kare? Sahi policy choose karne ke liye aapko apni needs aur budget dono ko dhyan me rakhna chahiye.

Important factors to consider: – Sum insured amount – Waiting period and exclusions – Network hospitals – Claim settlement process – Premium affordability

Tips: – Compare policy features carefully – Read policy documents before buying – Avoid choosing only on premium cost

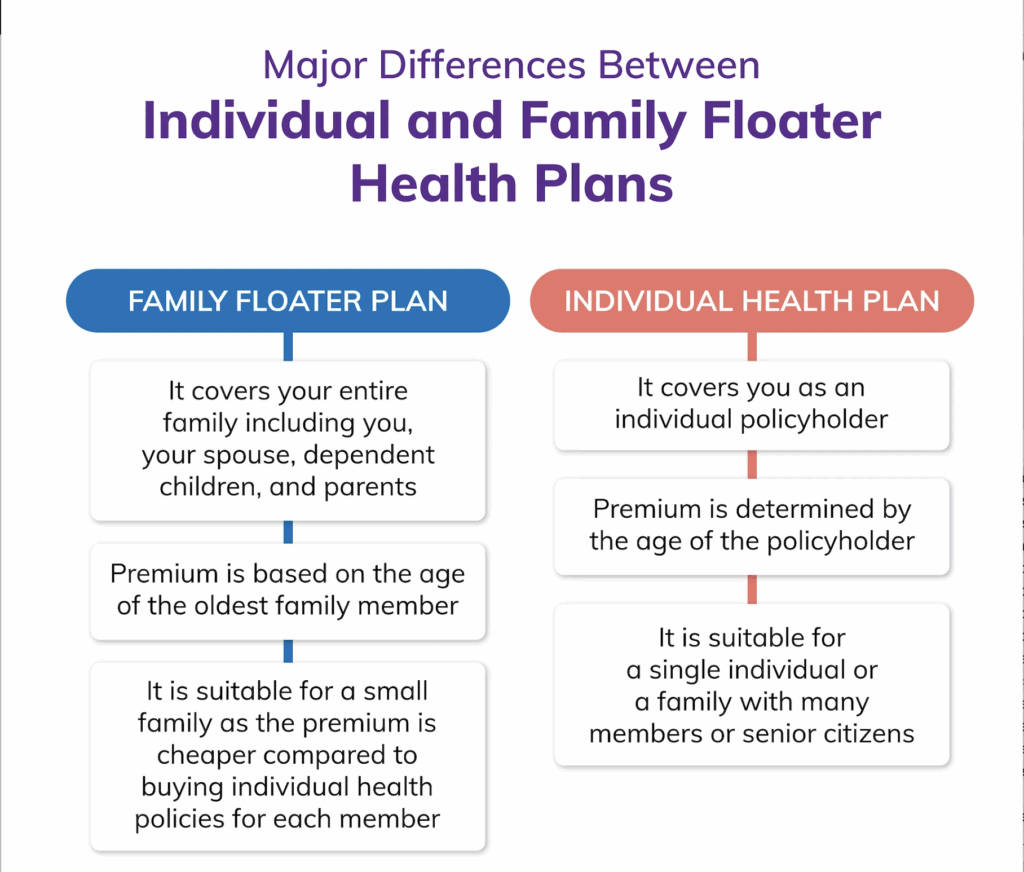

Individual and family floater health insurance are two common types of health insurance plans in India. Choosing the right one depends on your family size and financial goals.

Individual Health Insurance: – Covers a single person – Sum insured is fixed for that person – Premium is paid for one person only

Family Floater Health Insurance: – Covers the entire family under one policy – Sum insured is shared among all members – Premium is usually higher than individual but covers everyone

Difference summary: – Coverage: Individual → 1 person, Family Floater → multiple members – Premium: Individual → lower, Family Floater → higher but cost-effective per member – Claim: Individual → only insured person, Family Floater → any member

Important note: Always check policy terms, waiting periods, and exclusions before purchasing.

This article is for informational purposes only and does not provide insurance advice.

There are different types of health insurance plans in India, each designed to meet different medical and financial needs.

Understanding the types of health insurance plans helps you choose the right policy for yourself and your family.

1. Individual Health Insurance This plan covers medical expenses of a single person. It is suitable for individuals who want independent coverage.

2. Family Floater Health Insurance A family floater plan covers the entire family under a single policy. The sum insured is shared among all members.

3. Senior Citizen Health Insurance These plans are designed for people aged 60 years and above. They usually have higher premiums and specific coverage conditions.

4. Critical Illness Insurance This policy provides a lump-sum amount if the insured is diagnosed with a listed critical illness such as cancer or heart disease.

5. Group Health Insurance Offered by employers or organizations, group health insurance provides coverage to employees and sometimes their family members.

Important note: Coverage, exclusions, waiting periods, and benefits vary from insurer to insurer. Always read the policy document carefully before purchasing.

This article is for informational purposes only and does not provide insurance advice.

Health insurance is a financial protection plan that helps you cover medical expenses during illness, accident, or hospitalization.

Health insurance kya hota hai? Health insurance ek aisa insurance cover hai jo aapke hospital bills, treatment costs, medicines aur medical expenses ko cover karta hai.

In today’s time, medical costs in India are increasing rapidly. Even a short hospital stay can cost thousands or lakhs of rupees. Health insurance helps reduce this financial burden.

How does health insurance work? You pay a fixed amount called premium to the insurance company. In return, the insurance company covers eligible medical expenses as per policy terms and conditions.

Key benefits of health insurance: – Covers hospitalization expenses – Provides cashless treatment at network hospitals – Helps in managing unexpected medical costs – Offers tax benefits under Section 80D

Example: If you are hospitalized and the total bill is ₹2,00,000, your health insurance policy can pay the eligible amount directly to the hospital or reimburse you later.

Important note: Health insurance coverage depends on policy terms such as waiting period, exclusions, sum insured, and network hospitals.

This article is for informational purposes only and does not provide insurance advice.